The SEC Just Complicated Shareholder Engagement—Why? - Because it Can

The SEC Just Complicated Shareholder Engagement—Why? - Because it Can

Share This Email:

March 17th, 2025

Written by Frank Glassner, CEO

Veritas Executive Compensation Consultants

Ah, just in time for the peak of proxy season, the SEC has tossed a new wrench into the gears of shareholder engagement. Because what would corporate governance be without a little extra regulatory chaos?

On February 11, 2025, the SEC staff decided that the old playbook for passive investors was just too simple and—heaven forbid—working. So, they updated their Compliance and Disclosure Interpretations (C&DIs) on Schedule 13D/G filings, adding a fresh layer of uncertainty to investor engagement. The full fallout remains to be seen, but here’s what we know so far: major institutional investors are hitting the brakes on engagement with portfolio companies, just as boards and executives are gearing up for their busiest shareholder interactions of the year. Timing, as always, is impeccable.

The 13D/G Breakdown (or How We Got Here in the First Place)

For those who prefer not to spend their evenings poring over SEC filing requirements (I envy you), here’s the quick and dirty version:

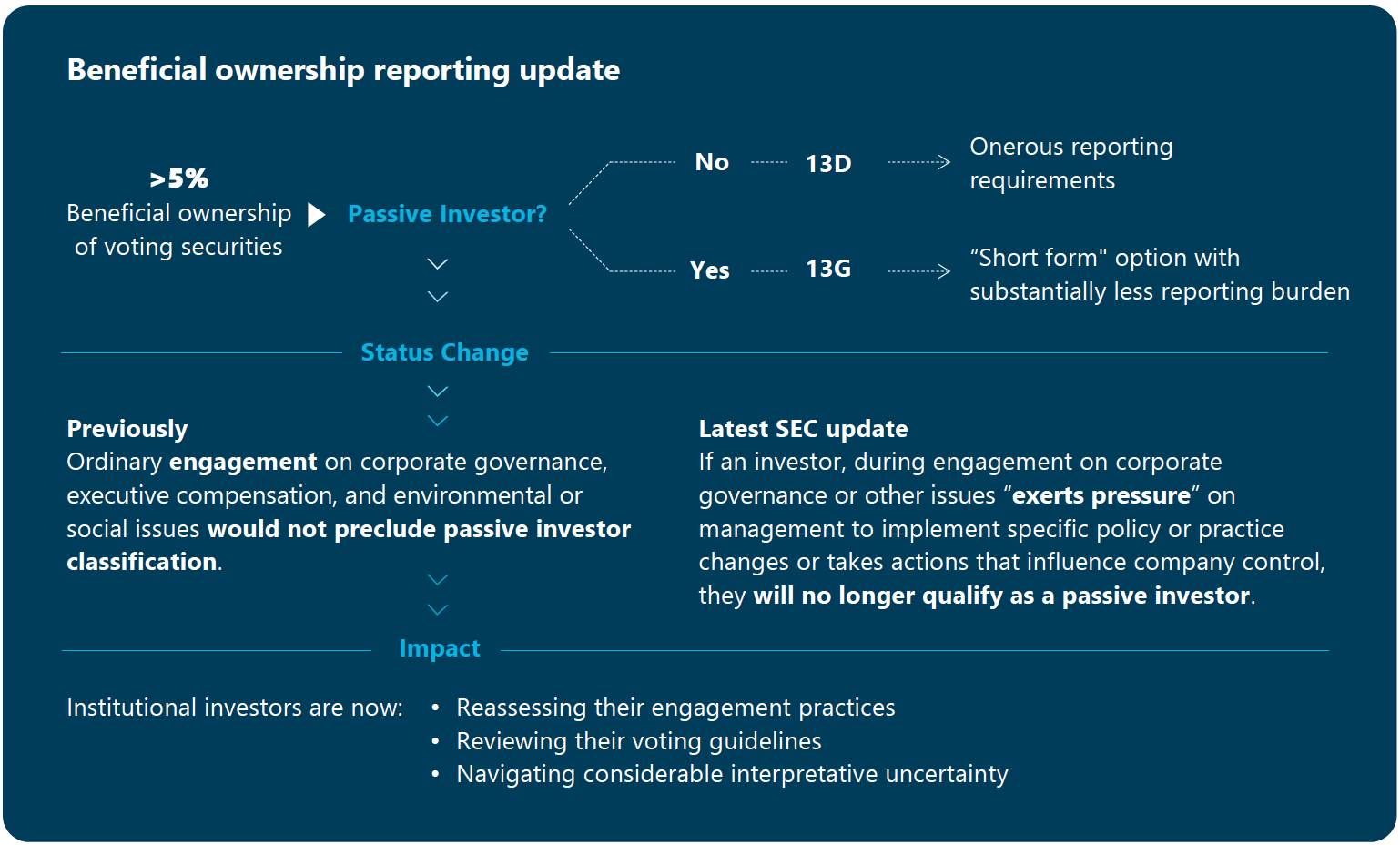

- Any shareholder who beneficially owns more than 5% of a company’s voting securities must report that ownership to the SEC.

- They can either file Schedule 13D, which is a full-disclosure headache, or Schedule 13G, a lighter, less intrusive alternative—if they qualify as a "passive investor."

- “Passive” traditionally meant not actively trying to control or influence the company’s direction—meaning large institutional investors like BlackRock, Vanguard, and Fidelity have long relied on this loophole to file the far easier 13G.

Until now. Here’s how it breaks down:

What Changed? (Spoiler: Everything and Nothing)

The SEC has redefined what it means to be a passive investor—and not in a way that makes anyone’s life easier. Under the new guidance, institutional investors may no longer qualify for 13G filings if they:

- Exert pressure on management to change policies or practices;

,or - Indicate they might withhold support for director nominees unless the company bends to their expectations.

Now, let’s pause for a moment and consider what institutional investors do for a living. Their whole business model is built on engaging with companies and pushing for changes they believe will maximize shareholder value. So, if BlackRock or Vanguard so much as implies that a company should adjust its governance policies, they may be forced to file the far more burdensome Schedule 13D—a paperwork nightmare they’re unlikely to embrace.

Naturally, instead of diving into that regulatory mess, some major investors have already decided to simply pause engagement efforts. That’s right—just when companies need shareholder dialogue the most, some of their largest investors may be ghosting them to avoid SEC headaches.

The Fallout: What This Means for Companies

As if proxy season weren’t already enough of a three-ring circus, here’s what you might be up against now:

- Radio Silence from Institutional Investors: If your biggest shareholders aren’t engaging, expect less clarity on where they stand on governance, compensation, and board matters.

- Less Flexibility, More Surprises: Without early conversations, companies may find themselves blindsided by investor pushback when it’s already too late to course-correct.

- A More Opaque Proxy Season: Investors might wait until proxy votes to make their grievances known—meaning companies will be left guessing rather than negotiating.

So, What’s the Move?

At Veritas, we know executive compensation and governance aren’t just about checking compliance boxes—they’re about staying ahead of these regulatory curveballs. The SEC’s new stance makes it more critical than ever to ensure your compensation plans, proxy disclosures, and governance policies can stand on their own merits—without relying on institutional investors to tell you what they think beforehand.

If your board and executive team want to get ahead of this mess—and avoid scrambling when shareholder silence turns into a full-blown voting revolt—let’s talk. We’re here to help you navigate the murky waters of executive compensation, governance, and regulatory chaos (because we know the SEC isn’t done playing this game).

Frank Glassner

CEO, Veritas Executive Compensation Consultants

|